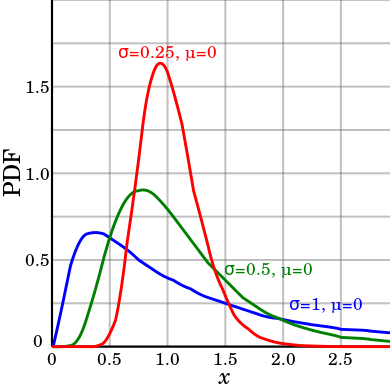

If \(Y=\ln X\) is a normal distribution, then \(X\) is log-normal.

\begin{equation*}

f(x;\mu,\sigma)=\frac{1}{\sqrt{2\pi\sigma} x}\exp\left(-\frac{[\ln(x)-\mu]^{2}}{2\sigma^{2}}\right)

\end{equation*}

for \(x\ge0\)

Note that \(\mu,\sigma\) do not represent mean or standard deviation of \(X\), but of \(\ln X\).

Mean: \(\exp(\mu+\frac{1}{2}\sigma{2})\)

Variance: \(\exp(2\mu+\sigma^{2})\left(e^{\sigma^{2}}-1\right)\)

\begin{equation*}

F(x;\mu,\sigma)=P(X\le x)=P[\ln(X)\le\ln(x)]=\Phi\left(\frac{\ln(x)-\mu}{\sigma}\right)

\end{equation*}

Usage

It is the result of the product of many independent random variables, each of which is positive (follows from the Central Limit Theorem). Useful for the accumulation of many small percentage changes.